| Francois Micheloud's Homepage | En FRANCAIS s'il vous plaît |

|

| .5.

Oligopolies, trusts and monopolies . |

|||

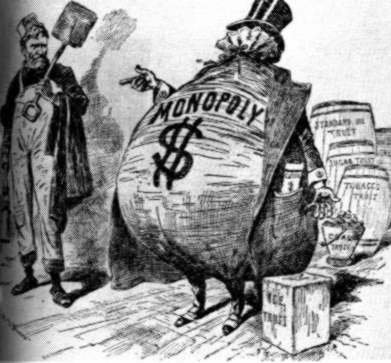

The first industrial pools in the 80's tried to fix the price of their goods (be it salt, whiskey, cattle, iron, oil ...) no matter the circumstances, to a level high enough to earn them a nice living, but not too high so as not to attract outside competitors. United they could also earn from the other side, by lowering costs. Railroads were forces to give them wholesale rebates, inefficient or poorly situated factories were closed, redundant workers could be laid off, and sometimes a war chest was even made. Outside competitors could generally not survive. Pools were in their eyes modernity, sweeping the cut throat competition that could only lead to ruin and introducing rational methods of production management. They could also invest in common scientific research and advertisement, and to organize buying centers. As they did not think of themselves as public benefactors, they underlined the exceptional wages in their factories and price stability. Sure, in periods of increasing demand their workers were paid more to be sure that they would not strike, but in normal time the pool allowed drastic wages decrease, as the owner of a striking factory could easily transfer his production in another factory. Did Rockefeller invent the trust ? (by trust we mean the industrial, not the juridical structure). Not really, and we need not look very far to find many other examples. In the North the pig people had set up a dead pig trust in Chicago. Continued on next column |

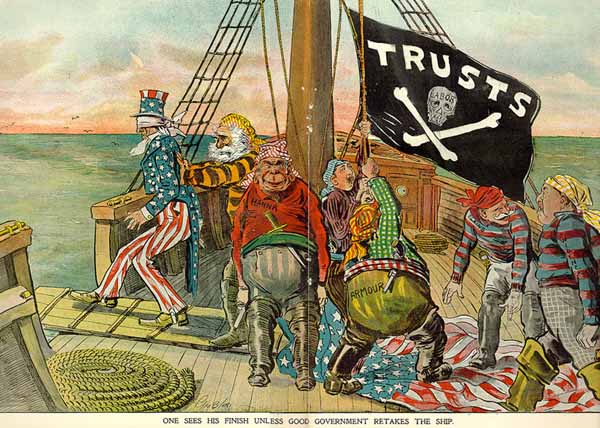

In the south, the sugar trust was already well established. In the east, steel baron Andrew Carnegie dominated the whole industry. As he used to say to his competitors, Remember, Gentlemen, I'm the lowest cost producer ! The biggest or most efficient producer could impose his will on the other industry members, and was king to the fragmented links up and downstream of the production chain. If one resisted, his business diminished quickly so as to put him totally out of the market and to allow that one who lead him to the verge of bankruptcy to buy him out for a dime. Price war was always an option for companies in the same production stage. As soon as bankruptcy had liquidated an dissident, price rose again to allow for a considerable profit, but never enough to draw new competitors. Profits were hoarded in war chest, in case of a new price war. The walrus moustached banker John Pierpont Morgan, probably the most powerful man of his time, did not like the disorders of natural competition either. He made many gigantic trusts himself, like United Steel, American Tobacco or General Electric, whose control was very centralized. Moreover, as is the case today in Switzerland, many boards were crossed, with members of the board sitting in different companies, which make oligopolistic deals easier. |

||

|

|||